Ductile Iron Pipe GCC Market 2024–2030: Demand Trends, Growth Drivers, and Main Risks

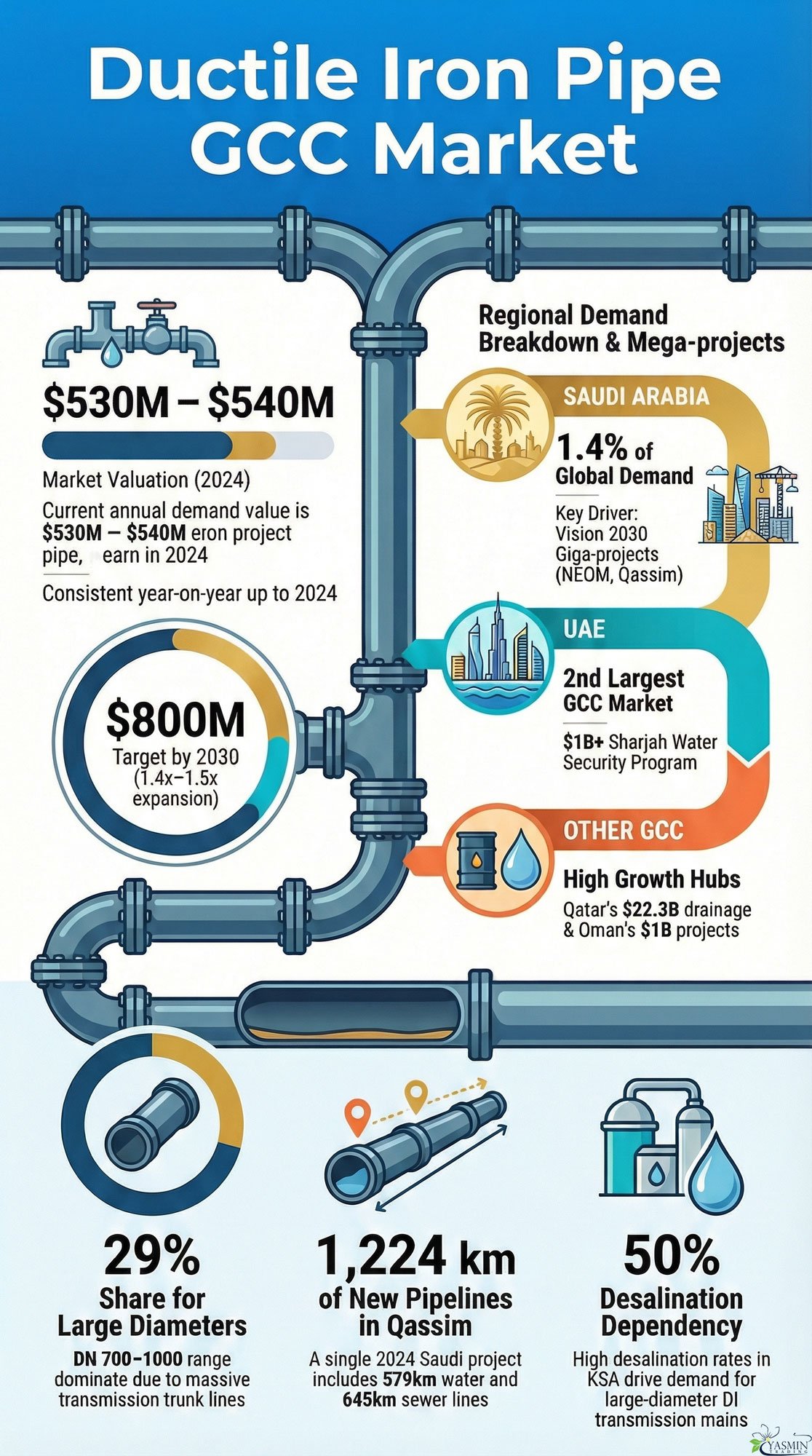

Ductile iron pipe GCC market forecast to reach such value at USD 530-540 million, with an expanding rate of about 1.4×–1.5× to project 750-800 million by 2030. This market represents Saudi Arabia and the UAE DI pipe demand as the most significant shares among the Cooperation Council of the Arab States of the Gulf. The main drivers of this market include desalination transmission mains, potable water distribution (GCC), and wastewater and sewage systems (GWI).

In this post, we’ll provide helpful information about market drivers, segmentations, market snapshot, and various aspects of this matter. Stay with us till the end.

Definition and Scope of the Market

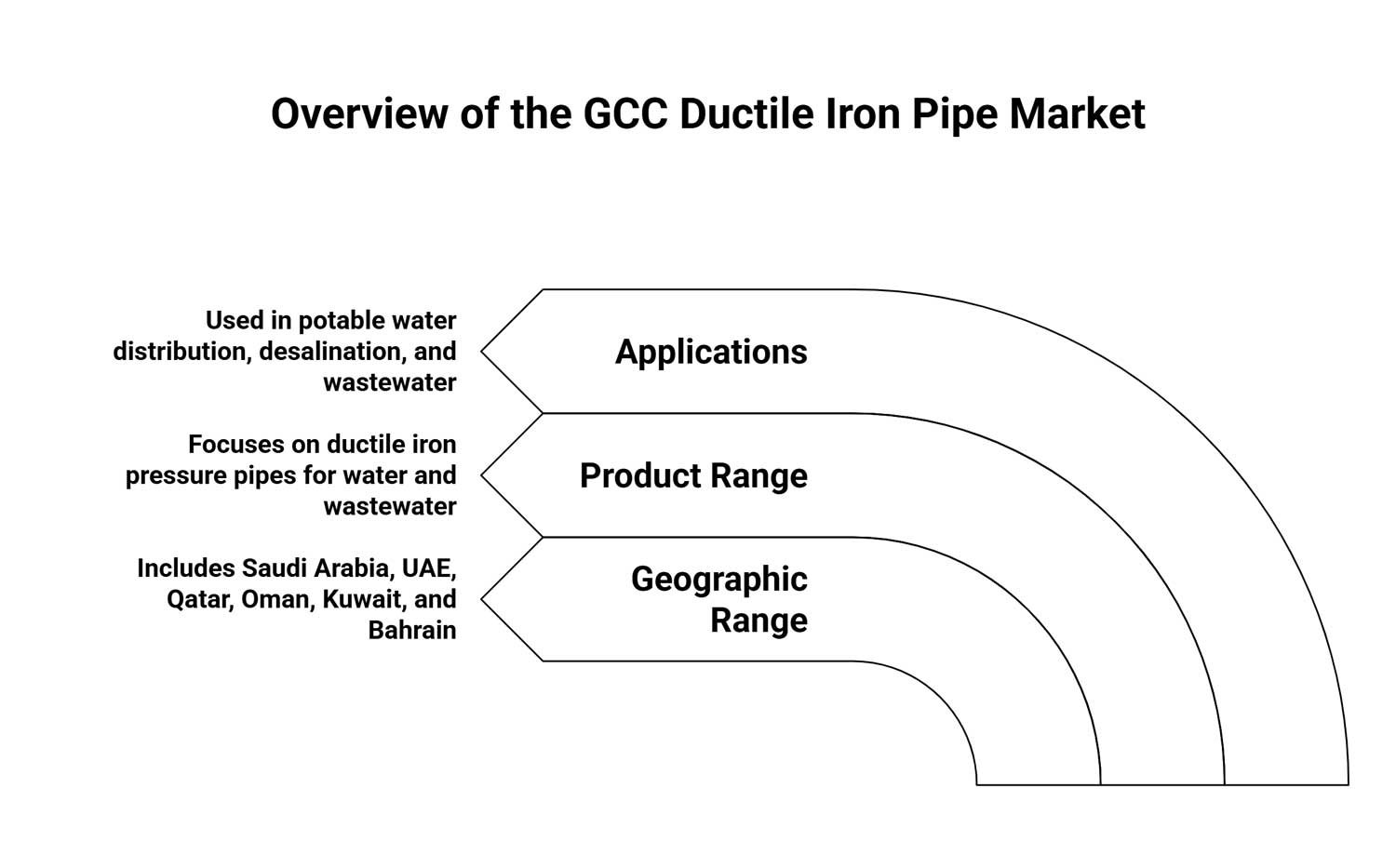

The GCC market for ductile iron pipes includes pressure pipes designed for high-demand water and wastewater applications in the six Gulf states.

Geographic Range

The Gulf Cooperation Council (GCC) includes Saudi Arabia, the United Arab Emirates, Qatar, Oman, Kuwait, and Bahrain. Every nation devotes a significant portion of its budget to water infrastructure, with Saudi Arabia and the United Arab Emirates having the largest shares (GWI).

Product Range

The emphasis is on ductile iron pressure pipes, which are utilized in:

- Distribution of potable water (GCC)

- Transmission mains for desalination (GCC)

- Wastewater and sewage force mains (GWI)

Generic cast iron and unprotected steel pipes are not included in this scope because they are not strong enough or have enough corrosion resistance for modern GCC utility requirements.

Market Snapshot for 2024–2025

With governments expanding vital water infrastructure, the ductile iron pipe market in the GCC is expected to grow at a mid-single-digit annual rate, with a 2024 valuation of approximately USD 530–540 million.

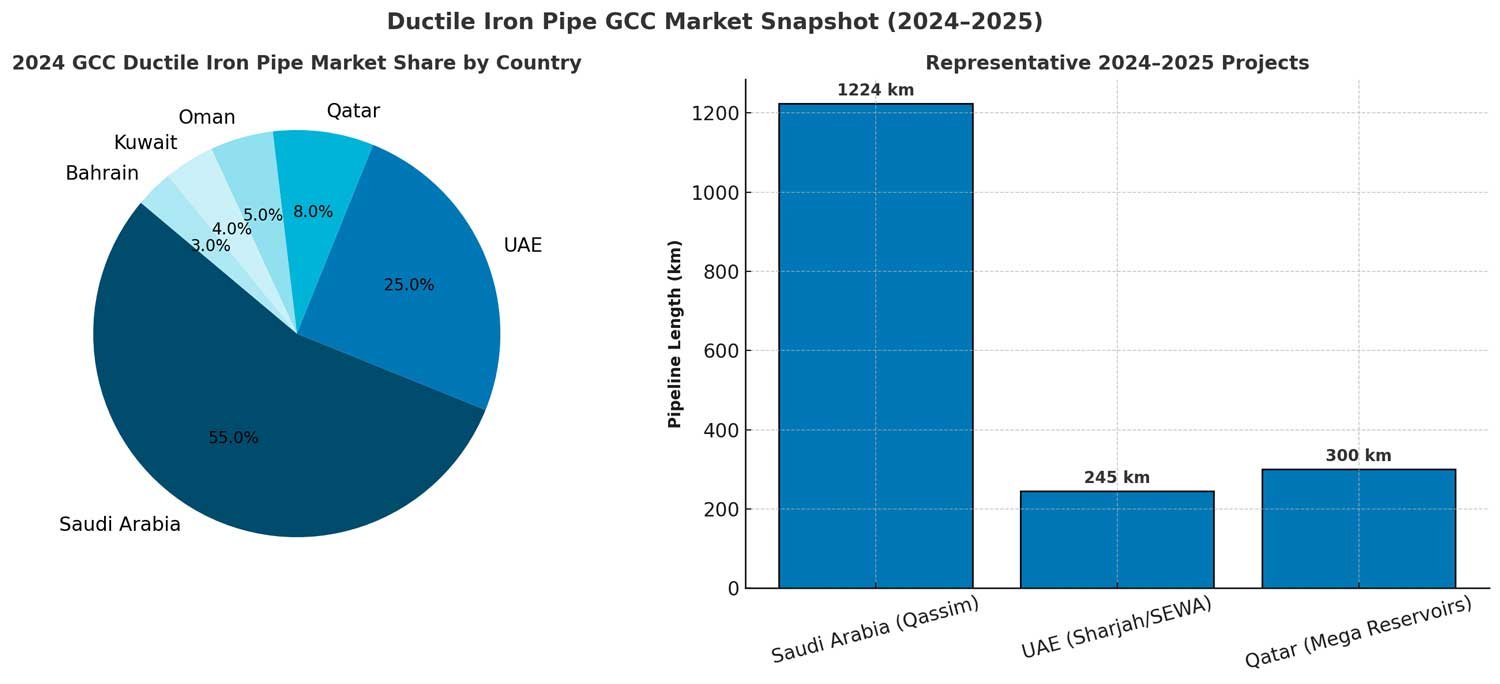

By the share of the country

Saudi Arabia leads with almost 1.4% of the world’s demand for ductile iron, helped along by the expansion of water and sanitation in Vision 2030.

Additionally, due to transmission improvements and water security initiatives, the UAE comes in second.

Through continuous national water projects and investments in urban networks, Qatar, Oman, Kuwait, and Bahrain all make contributions.

Typical projects from 2024 to 2025

- Saudi Arabia, Qassim: 16 new contracts strengthen service coverage by encompassing 645 km of sewer lines and 579 km of potable water pipelines.

- UAE, Sharjah: Water security is strengthened by nearly 245 km of 1600 mm DI transmission mains between the UAE and Sharjah.

- Mega Reservoirs in Qatar: Resilience and the storage of potable water are still supported by large-diameter DI foundations.

When taken as a whole, these initiatives show how the GCC’s robust investment pipeline is influencing short-term growth.

Demand Drivers in the GCC

There are four primary directions that lead the ductile iron pipe GCC market for those regional water infrastructure systems.

Potable Water Distribution (GCC)

These pipe networks shape the largest share of ductile iron pipe use cases. In Saudi Arabia, the UAE, and Qatar, urban growth forced the use of trunk mains and transfer lines in cities to handle a reliable supply.

Desalination Transmission Mains (GCC)

As half of the world’s desalination capacity is centered in the Gulf area, ductile iron pipes are responsible for moving water inland, while decreasing the need for single sources by interconnected grids.

What effect does urbanization have on the demand for DI pipes?

There is pressure to update water networks due to the fast growth of cities. In order to reduce leakage through NRW reduction programs and increase service life, governments invest in replacing old cast iron and steel mains with DI systems.

In what ways do policies speed up the growth of networks?

More exhaustive service coverage is required by strategic visions like Saudi Vision 2030 and comparable national water strategies in the United Arab Emirates, Qatar, and Oman. These regulations ensure that there will always be a need for DI pipelines in desalination, wastewater, and potable water projects.

Market Segmentation of Ductile Iron Pipe GCC Market

The ductile iron pipe GCC market is segmented by applications, technical aspects, and country-level components. This type of segmentation helps to clarify how the current demand will change in the future.

By Application: Where Does Demand Concentrate?

The largest share goes to potable water distribution (GCC) that shapes the long transferring lines in cities and urban supply grids by DI pipelines in Saudi Arabia, the UAE, and Qatar.

While sewage and wastewater force mains include such fast growth in deep-tunnel feeders and high-pressure mains that are resistant to hydrogen sulfide (H2S). (Source: CTFassets)

Furthermore, industrial and power systems use DI pipes for cooling, process, and fire networks where high temperature tolerance matters the most. Also, for irrigation, treated sewage effluent (TSE) networks are used for designing the reuse strategies.

| Application | Drivers | Challenges | Market Relevance |

|---|---|---|---|

| Potable Water | Urban growth, inter-city transfer, reliability needs | High capital cost for trunk mains | Largest share; backbone of GCC DI demand |

| Wastewater | Sanitation expansion, NRW reduction programs | H₂S corrosion in sewer environments | Fastest growth; vital for sewage & drainage networks |

| Industrial/Power | O&G cooling, process, fire protection networks | Harsh operating conditions, reliability | Stable niche in energy and industrial infrastructure |

| TSE Reuse | Water scarcity, irrigation reuse policies | Quality assurance, cost-effectiveness | Emerging segment; aligned with GCC sustainability goals |

By Diameter and Pressure Class: How Do Specs Shape Demand?

One-third of MEA ductile iron demand is for large diameters up to DN 700-1000, which is right for trunk mains of GCC. Additionally, pressure classes can define how these pipes are used: high-pressure classes for long-haul transmissions and low-pressure classes for distribution systems.

By Lining and Protection

In this case, DI pipes are coated with epoxy or a barrier and include such cement mortar lining for corrosion resistance in harsh environments. Global standards such as ISO 8179 fulfill zinc coating requirements and PE encasement for aggressive conditions.

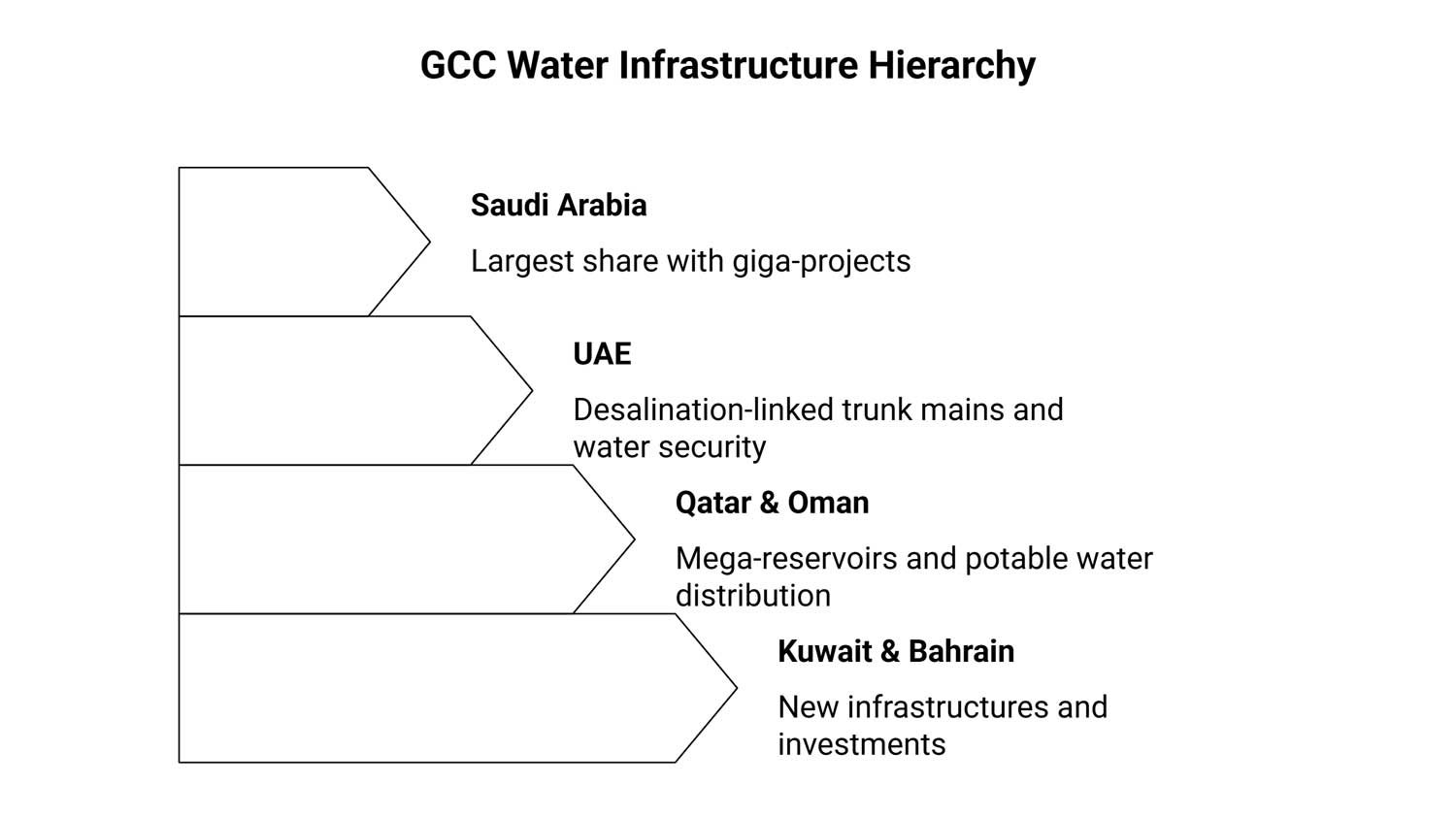

Country-Level Outlook: Which States Drive Projects?

- Saudi Arabia has the largest share with giga-projects (under Vision 2030), with the Qassim networks project.

- The UAE, mainly known for its desalination-linked trunk mains and SEWA water-security transmission.

- At the next level, Qatar, with mega-reservoirs and deep-tunnel drainage programs, and Oman, with Nama water in potable water distribution, take place.

- At last, Kuwait, with brand-new infrastructures and Bahrain, with over $2 billion investment on water and power systems through 2026, complete the market of DI in GCC.

What Defines Ductile Iron Pipe Prices in the GCC?

The ductile iron pipe GCC market revolves around the universal iron and steel cycles, which represent how changing prices will decrease the margins due to the growth of billet costs and some limitations in EPC contractors’ abilities.

The supply roots in both regional and international manufacturers. According to the Research and Markets, Saudi Arabia and the UAE, on the local side, and China, India, and Europe, on the global side, provide the supply sources. Additionally, shipping rates and tariffs made imports less competitive than the benefits for local suppliers.

Lastly, competitive tendering surpassed procurement that typically comes from strict rules of utilities and local manufacturers to control the supply-demand balance. Despite these restrictions, it seems the local market is about to reach such growth and development in regional supply chains due to the 2030 outlook.

Check the table below for a quick view of ductile iron pipe pricing factors:

| Factor | Implication | Takeaway |

|---|---|---|

| Materials | Steel price swings squeeze margins | Costs stay volatile |

| Supply | Local (KSA/UAE) plus imports (Asia/Europe) | Balance global + local sources |

| Logistics | Freight and tariffs weaken imports | Local makers gain advantage |

| Tendering | Strict rules limit pricing flexibility | Thin margins, quality matters |

| Outlook | Vision 2030 supports localization | Long-term resilience likely |

Competitive Landscape & Supply

The landscape of the ductile iron pipe GCC market is founded on local manufacturers of Saudi Arabia and the UAE, whose growth decreases the need for imports.

Regional manufacturers create this opportunity to link production to the next chain through contractors and distributors in EPC.

With global standards like ISO and AWWA, coating quality, pressure-class variety, and diameter ranges are aligned to reach the best match. Utilities and EPCs design such compliances and rules for potable water, desalination mains, and water networks that keep the authenticity and uniformity in the final production.

Forecast 2025–2030 of DI Pipe GCC Market

The ductile iron pipe GCC market is projected to reach such a mid-single-digit CAGR by 2030 due to significant investments in potable water distribution, desalination transmission mains, and wastewater systems.

- Future Insight: At the end of this decade, demand will experience such growth at a rate of 1.4 to 1.5 in its 2024 value. This rise comes from a related project to Vision 2030 in desalination grids and mega-reservoirs.

Although this growth is sensitive to the volatility of prices in both raw materials and transportation, it can be developed by improvements in tendering and financial processes.

Policy, Regulation & Standards

The development of the ductile iron pipe GCC market is dependent on policies and standards in order to form uniform product specifications.

National Visions and Public-Health Directions

Saudi Arabia’s Vision 2030, UAE Water Supply programs, and other projects show the wide service range and decrease in NRW KPIs. Also, stable demand for ductile iron pipe is confirmed by these restrictions in wastewater, desalination, and potable water systems.

Standards define how specifications are designed.

Project procurements are planned by standards such as ISO and AWWA, for instance, ISO 8179 shapes the coatings specs, pressure classes, and linings for reliable networks over decades.

Procurement Frameworks and Localization

The governments of Saudi Arabia and the UAE consider exceptional capacity for the local production that influences suppliers by offering rewards to follow compliance and contribute to the consistency of the next regional chains.

| Focus Area | Essentials | Impact |

|---|---|---|

| National Mandates | Vision 2030, water security targets, NRW reduction | Drives steady DI pipe demand |

| Technical Standards | AWWA & ISO rules, ISO 8179 zinc coating adoption | Ensures uniform quality and reliability |

| Procurement & Localization | Local production preference, tender rules for compliance | Strengthens supply chain, lowers import reliance |

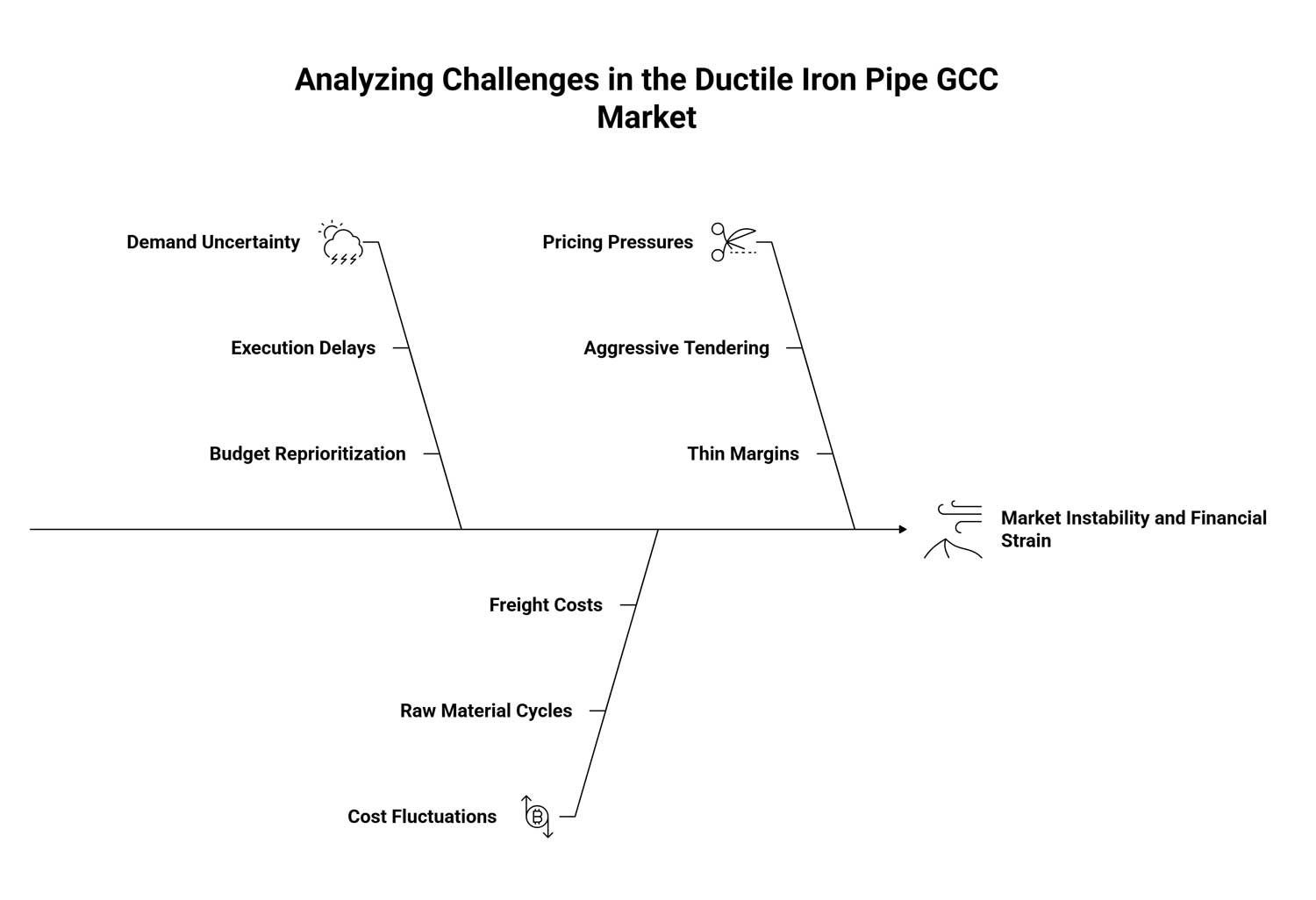

Probable Risks and Challenges in Ductile Iron Pipe GCC Market

If not handled carefully, a number of risks facing the GCC market for ductile iron pipe could cause demand patterns to shift, margins to tighten, and project pipelines to be delayed.

How Can We Make Sure That Projects Will Be Finished on Time and on Budget?

Uncertainty regarding year-to-year demand is caused by execution delays and changing national budget priorities. Procurement pipelines are frequently altered by reprioritization windows that affect mega-projects.

How To Control Costs?

The market is vulnerable to abrupt fluctuations in prices due to iron and steel raw material cycles. (Source: CognitiveMarketResearch) Growing freight costs put additional pressure on the economics of imports, particularly when international shipping is disrupted.

What Are the Main Dilemmas in the Pricing Environment?

In the GCC, aggressive tendering restricts flexibility and puts constant pressure on prices by forcing suppliers to operate on thin margins.

Opportunities and Strategic Moves

The ductile iron pipe GCC market includes such growth for suppliers and EPCs that can plan an improvement program for other regional components and technical requirements.

Where Can Scale Make the Biggest Difference?

In a high-value project, large-diameter pipelines for transmission and desalination grids will provide water security in the following years.

How Can Wastewater Challenges Become Opportunities?

As highlighted in GrandViewResearch, in harsh environments that have H2S or in reuse corridors of TSE, they may provide some practical solutions to fulfill long-term opportunities in wastewater and desalination systems.

Smart Partnership in Ductile Iron Pipe GCC Market

Having such intimate partnerships with utilities and EPCs will pave the way for accessibility via standards and guidelines of coatings and linings for durable and resistant pipelines in GCC tenders.

Conclusion

The ductile iron GCC market has such fast growth compared to its competitors. This market includes three main drivers: potable water distribution, desalination expansion, and wastewater reuse. Local manufacturing, following global standards, and innovative partnerships provide such an excellent opportunity to speed up this growth. While there are several probable risks, such as volatility of raw material process and delays with threats, this dynamic market is about to experience stability by 2030.

FAQs

1- What is the forecasted value of the GCC ductile iron pipe market by 2030?

Ductile iron pipe GCC market forecast to reach such value at USD 530–540 million, with an expanding rate of about 1.4×–1.5× to project 750–800 million by 2030.

2- Which countries hold the most significant shares of DI pipe demand in the GCC?

This market represents Saudi Arabia and the UAE DI pipe demand as the biggest shares among the Cooperation Council of the Arab States of the Gulf.

3- What are the main drivers of this market?

The main drivers of this market include desalination transmission mains, potable water distribution (GCC), and wastewater and sewage systems (GWI).

Leave a Reply